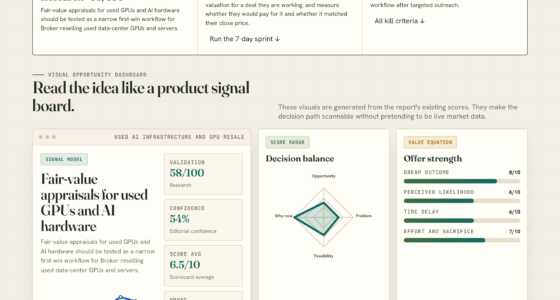

📊 Full opportunity report: The $725 Billion Question: Hyperscaler Capex Q1 2026 and What the Earnings Don’t Answer on ThorstenMeyerAI.com — validation score, market gap, and execution plan.

TL;DR

The world’s largest hyperscalers reported a combined $725 billion in AI-related capital expenditure for 2026, a 69% increase over 2025. Despite strong spending, market reactions to NVIDIA’s stock suggest doubts about the immediate revenue impact and future returns.

On April 29, 2026, Microsoft, Amazon, Alphabet, and Meta announced a combined AI infrastructure capital expenditure of approximately $725 billion for 2026, marking the largest investment cycle in modern tech history. This surge underscores the industry’s focus on AI development, but market reactions, especially to NVIDIA’s stock, highlight uncertainties about the actual revenue and profit impact of such spending.

The four hyperscalers reported a 69% year-over-year increase in AI capex, totaling around $700-725 billion, with Morgan Stanley estimating the global AI infrastructure investment at $740 billion. Microsoft plans to spend about $190 billion, Amazon $200 billion, Alphabet $185 billion, and Meta between $125-145 billion. These figures significantly outpace previous years, with capex as a percentage of revenue rising from 10-15% pre-AI to roughly 25-30% in 2026. The spending is not discretionary; these companies are committed to building AI infrastructure regardless of short-term ROI. Despite this, NVIDIA’s stock declined after its Q4 fiscal 2026 earnings, raising questions about whether GPUs remain the primary bottleneck for AI deployment or if other factors—such as power, cooling, or in-house silicon—are becoming limiting factors.$725 billion. The question capex doesn’t answer.

April 29, 2026. Largest capital-expenditure cycle in modern tech history. Lock-in across the Big Four.

Microsoft $190B. Amazon $200B. Alphabet $185B. Meta $125-145B. Up from $670B high-end consensus going in. +69% YoY surge over 2025. NVIDIA fell on the news. The structural questions — depreciation, power, in-house silicon, demand-pull, geopolitical — resolve through 2027-2028.

Four hyperscalers. $725B committed.

Each hyperscaler beat-and-raised in the same 24-hour window April 29. Microsoft / Amazon / Alphabet / Meta. The capex commitment is non-discretionary at this scale — companies cannot back out without creating asset write-downs and capacity gaps.

AC Infinity AIRPLATE S7, Quiet Cooling Fan System 12" with Speed Control, for Home Theater AV Cabinets

An ultra-quiet UL-certified fan system designed for cooling cabinets that requires minimal noise.

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Three paths. One question.

The capex buildout resolves through one of three structural paths. The honest assessment: the demand signals are real, the supply signals are real, and the balance between them is the structural question.

- Demand +60-100% YoYEnterprise translates fully.

- Utilization 85%+NVIDIA pricing power holds.

- $2.8T by 2028Jensen trajectory matches.

- No impairmentCapex fully accretive.

- Outcome: Multiples expand. Foundation for next decade.

- Demand +30-60% YoYPartial translation.

- Utilization 75-85%Weaker pockets visible.

- NVDA decel 75% → 30-50%Manageable adjustment.

- $30-80B impairmentLimited 2028 cycles.

- Outcome: Multiples compress modestly. No crisis.

- Demand +15-30% YoYEnterprise falls short.

- Utilization 65-75%Capacity glut visible.

- $150-300B impairmentBig Four 2027-2028.

- NVDA sharp decelPricing compression.

- Outcome: 30-50% multiple compression. Post-2001 telecom analog.

HP NVIDIA Tesla M60 16GB Server GPU Accelerator Processing Card 803273-001

16GB

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Five vectors. Interdependent.

Capital-allocation risks of this magnitude resolve through specific structural channels. The vectors are not independent — power constraints delay deployment which compresses utilization which triggers impairment.

Capital intensity has reset upward as the new baseline for tech-platform leadership. The competitive moat is partly capital availability rather than purely product or technology innovation. Tech-platform leadership now requires capital-deployment scale that fewer companies can execute.

CablesAndKits – 3 Prong AC Power Cord (6ft) 1.82m – 15A/125V, 14 AWG | 5-15P to C19, (NEMA 5-15P to IEC-60320-C19) | Heavy Duty Power Cable for Servers, Network and Data Center Needs – (Black)

MULTIPLE DEVICE COMPATIBILITY: This 3 prong AC power cord with NEMA 5-15P to C19 connector is ideal for…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Four assignments. By role.

Reset on structural pricing-power compression.

Bull case requires NVIDIA to maintain addressable share through FY27-FY28; in-house silicon migration argues that share compresses. Position accordingly. Consider AMD, Broadcom, downstream networking suppliers as partial substitutes that may benefit from compression. Stop pricing the $2.8T-by-2028 ceiling literally.

Treat capex as tailwind and risk factor.

Microsoft best-positioned through capacity-constrained Azure demand. Alphabet best-positioned through TPU silicon independence. Amazon best-positioned through Trainium/Inferentia revenue diversification. Meta most exposed through internal-product-only revenue offset. Position differentially rather than treating Big Four as equivalent.

Use the buildout to negotiate.

Capacity becoming abundant; pricing under structural pressure. 2-3 year contracts with capacity guarantees + price-discount escalators that capture unit-cost reduction as buildout absorbs. Multi-cloud sourcing more attractive as capacity scarcity ends. The negotiating window opens through 2026-2027.

Plan for capacity glut by H2 2027.

Capex commitment produces more compute than current demand absorbs at current pricing. API pricing pressure compounds through 2027-2028. China sphere cost gap (5-30× cheaper) makes more acute. Margin guidance for next 18 months should explicitly model capacity-driven price compression. Hedge accordingly in S-1 disclosures.

AI Hardware Engineering: Designing GPUs, TPUs, and Neural Processing Units for High-Throughput Machine Learning Workloads (AI Infrastructure, Hardware & Compiler Engineering Series)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Implications of Record-Breaking AI Investment

This level of AI-related capital expenditure could influence the future revenue and profit landscape of the tech industry. While the investment indicates confidence in AI’s long-term potential, market responses suggest uncertainty about the immediate financial returns. Factors such as in-house silicon development and infrastructure constraints may impact the realization of expected benefits, potentially affecting financial performance in the coming years. These developments highlight the importance of monitoring how these investments translate into operational and financial outcomes.Historical and Market Context of AI Infrastructure Spending

Over the past decade, hyperscalers have gradually increased their AI-related investments, but the first quarter of 2026 marks a significant escalation. The combined $725 billion exceeds previous annual capex levels and reflects a strategic shift toward AI as a central growth driver. Historically, annual capex was often below 20% of revenue; now, it has increased notably at many firms. The focus on GPU and silicon investments, including Alphabet’s TPU v6 and Amazon’s Trainium chips, indicates efforts to reduce dependence on external hardware providers like NVIDIA. Market skepticism is exemplified by NVIDIA’s stock decline despite record data center revenues, raising questions about the immediate return on these investments and whether current infrastructure can support the anticipated AI workload growth.

“Our AI chip investments remain largely on track, and the $200 billion capex plan continues to guide our strategy for 2026.”

— Amazon CEO Andy Jassy

Uncertainties Surrounding AI Capex Effectiveness

While hyperscalers have committed substantial capital to AI infrastructure, questions remain about whether these investments will result in the anticipated revenue and profit growth. Uncertainties include potential bottlenecks such as GPU availability, power and cooling limitations, and the development of in-house silicon like Google TPU v6 and Amazon Trainium. The market’s negative reaction to NVIDIA’s stock suggests skepticism about the immediate impact of increased capex on earnings, and there is concern that revenue growth may not meet expectations in the coming years, potentially leading to impairments.

Monitoring Revenue Growth and Infrastructure Efficiency

Investors and industry analysts will observe how hyperscalers translate their significant capital expenditures into revenue growth, especially in AI services. Key indicators include the progress of in-house silicon development, improvements in power and cooling efficiency, and utilization rates of new infrastructure. NVIDIA’s future earnings and market share will also serve as indicators for GPU demand and the broader AI hardware ecosystem. Upcoming quarterly reports and earnings calls will provide insights into whether these investments are beginning to generate the expected financial returns or if structural challenges will delay or diminish their impact.

Key Questions

Why did NVIDIA’s stock fall despite record data center revenues?

Market concerns about whether GPUs remain the primary bottleneck for AI deployment or if other factors like power, cooling, or in-house silicon are becoming limiting constraints contributed to the stock decline, despite strong revenue figures.

Are hyperscalers likely to cut back on AI capex if revenue growth slows?

Given the current commitments and strategic importance of AI infrastructure, hyperscalers are unlikely to reduce their capex in the near term. The investments are considered strategic, but efficiency gains and actual revenue realization will be important factors to monitor.

What risks do these record-high investments pose for future profitability?

The main risks include potential revenue shortfalls if infrastructure investments do not translate into proportional earnings, and the possibility of impairments if revenue growth stagnates or declines in subsequent years, especially as depreciation schedules impact financial statements.

How might in-house silicon affect the AI hardware market?

Development of in-house silicon such as Google TPU v6 and Amazon Trainium could influence market dynamics by reducing dependency on external providers like NVIDIA. This shift may impact pricing, supply chains, and competitive positioning, but the speed and scale of deployment remain uncertain.

Source: ThorstenMeyerAI.com