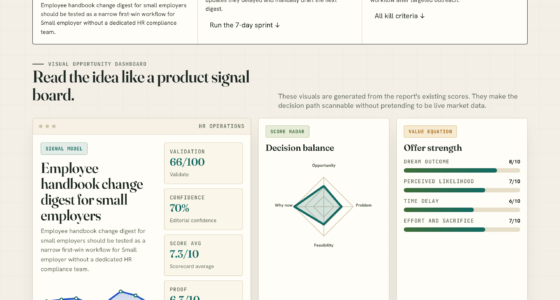

📊 Full opportunity report: The mandate. Why the US conversational- finance surface does not translate to Europe. on ThorstenMeyerAI.com — validation score, market gap, and execution plan.

TL;DR

The US and Europe have fundamentally different approaches to open finance. The US’s permissionless model contrasts with Europe’s mandated, license-based system, affecting how conversational finance surfaces are built and operated.

OpenAI’s launch of its personal-finance surface in the US on May 15, 2026, was permissionless—companies used API keys and aggregated data without licensing or regulatory approval. In contrast, Europe’s regulatory regime treats similar data access as a licensed, consent-based activity, preventing a straightforward US-style rollout.

In the US, the personal-finance surface was built atop a permissionless, private infrastructure—Plaid’s API access—allowing rapid deployment without regulatory hurdles. European law, however, mandates a licensing regime rooted in the open-banking directives PSD2 and PSD3, and the open-finance regulation FIDA, which extend licensing and consent requirements to a broader set of financial data, including investments and loans. These rules mean that any European equivalent of the US surface must be a licensed, consent-driven product, not a permissionless API aggregation.

Furthermore, the EU’s AI Act classifies financial AI systems, such as credit scoring models, as high-risk, imposing strict obligations supervised by regulators like BaFin. This layered regulatory environment transforms the architecture of financial surfaces, making compliance integral to their design. As a result, European firms building similar conversational finance tools must navigate a complex landscape of licenses, consent dashboards, conformity assessments, and AI classifications—factors absent in the US model.

The mandate.

Why the US conversational-

finance surface does not

translate to Europe.

data, AI — vs zero in the US build

maximum penalty

mandate — is likely operational

bank data · it is a licensed activity

- Access built by private aggregators — Plaid, Yodlee, MX, Finicity

- No banking license required to read bank data

- Read-only design sidesteps money-transmission rules

- No single federal open-banking statute · the surface ships as a product

- Access is a licensed activity — AISP / PISP under PSD2

- Regulator authorization required; no permissionless route

- Explicit, revocable, SCA-governed consent regime

- A directly-applicable rulebook (PSR) · the surface must be licensed

The architecture diverges at the foundation: the American surface treats account access as a product you buy and consent as a button you tap, while Europe treats both as mandates you are licensed and supervised to fulfill. In the US, you ship a finance surface. In Europe, you license one.Thorsten Meyer · The Mandate · Agentic Commerce 03

Implications of Regulatory Architecture on Market Access

This difference in regulatory architecture fundamentally alters market entry, product design, and competitive advantage. In the US, the permissionless environment favors agile, unlicensed aggregators that can quickly deploy new features. In Europe, the licensing and consent framework acts as a barrier to entry, favoring established, licensed players and potentially leading to slower innovation and more concentrated market power. This shift raises questions about consumer choice, innovation speed, and the potential for a more secure, privacy-respecting financial ecosystem.

European open banking API integration tools

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Regulatory Foundations of US and European Open Finance

The US’s open banking approach emerged from private sector initiatives like Plaid, with minimal regulatory oversight, enabling permissionless access to bank data. Conversely, Europe’s PSD2, enacted in 2018, and its successor PSD3, along with the FIDA regulation, establish a legal framework requiring licensed third-party providers to access financial data through regulated APIs. These frameworks aim to enhance security, privacy, and consumer control but create a fundamentally different environment for deploying financial surfaces.

Additionally, the EU’s AI Act, finalized in 2026, classifies certain AI systems as high-risk, imposing compliance obligations that influence the development of AI-driven financial tools. The combined effect of these regulations is a layered, mandate-driven architecture that contrasts sharply with the US’s permissionless API-driven model.

“The structural difference is that Europe treats account access as a mandate—licensed, consented, regulated—while the US sees it as a permissionless API. This fundamentally changes how financial surfaces are built.”

— Thorsten Meyer

Compatibility of Subscription-Based Models with Article 5(2) of the DMA: Case Study: Commission v Meta Platforms Inc. (Arbeitsberichte zum Informations-, Telekommunikations- und Medienrecht)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Unclear Impact on Consumer Experience and Innovation

It remains uncertain whether Europe’s mandated, license-based approach will lead to better consumer outcomes or slower innovation compared to the US permissionless model. The long-term effects on market competition, data security, and user privacy are still being observed and debated.

EU AI Act Compliance for HR Tech Founders: The Non-EU Founder's Implementation Guide — Bias Audit Templates,Conformity Assessment Checklists & 90-Day Sprint for AI-Powered Hiring Systems | 2026 Edit

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Expected Regulatory and Market Developments in Europe

Regulatory agencies in Europe are expected to finalize and enforce the PSD3, FIDA, and AI Act provisions in 2026-2027. European firms are preparing to build licensed, consent-driven financial surfaces, while US firms continue to operate permissionlessly. Cross-Atlantic regulatory dialogues and market entries will shape how these architectures evolve and influence global standards for open finance.

PSD2 compliant banking data aggregator

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Key Questions

Why can’t the US permissionless finance surface be directly implemented in Europe?

Because European law mandates licensing, consent, and regulatory compliance for data access, making a permissionless API-based approach legally and practically infeasible.

How does the EU’s AI regulation affect financial AI systems?

The AI Act classifies certain financial AI systems as high-risk, imposing strict obligations for transparency, safety, and supervision, which influence how these systems are developed and deployed.

Will Europe’s licensing approach slow down innovation?

It is possible, as licensing and consent processes introduce additional steps and costs. However, it may also lead to more secure and privacy-respecting products in the long term.

Who are the main players capable of building the European version of the US finance surface?

Licensed, consent-native financial institutions and specialized fintech firms with regulatory approval are best positioned to develop compliant European surfaces.

What are the implications for US firms expanding to Europe?

US firms must adapt their architecture to meet licensing, consent, and AI regulation requirements, which may involve significant re-engineering and strategic shifts.

Source: ThorstenMeyerAI.com