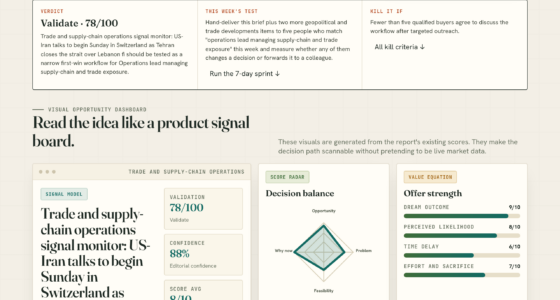

📊 Full opportunity report: The labor share. Is value really moving from labor to capital? The data isn’t on anyone’s side yet. on ThorstenMeyerAI.com — validation score, market gap, and execution plan.

TL;DR

The debate over AI’s impact on labor’s share of income remains unresolved. While aggregate data shows stability over 70 years, early marginal signals suggest shifts at the edges, leaving the true long-term effect uncertain.

Current data shows that the overall labor share of income in the US has remained within a narrow range over the past 70 years, despite technological upheavals like AI, raising questions about whether value is truly moving from labor to capital.

For seven decades, the US labor share has fluctuated between approximately 57% and 64%, indicating relative stability despite major technological advances such as automation, computers, and the internet. A recent Stanford study found a 13% decline in employment among 22-to-25-year-olds in AI-exposed roles since late 2022, suggesting early signs of displacement at the margins, particularly in routine and entry-level jobs. These findings present a complex picture: while the aggregate data suggests stability, localized signals point toward a shift in how value is distributed.

The core debate centers on whether these marginal signals will eventually influence the broader economy or remain isolated. Experts acknowledge that the current evidence supports both views—some argue the stable long-term trend indicates no significant redistribution, while others see early indications of AI beginning to reallocate returns toward capital, especially at the margins. The data is clear that the overall share has not yet changed, but the early displacement signals are real and consistent with theoretical predictions of an AI-driven shift.

The labor share.

Is value really moving

from labor to capital?

The data isn’t on

anyone’s side yet.

the skeptic’s strongest chart

in AI-exposed jobs since 2022 (Stanford)

declining labor share (Minniti et al.)

confirmable only in retrospect

The empirical ambiguity that weakens a confident displacement narrative is precisely what strengthens the case for a response that doesn’t require the narrative to be confident. You don’t need the premise proven to justify a no-regrets response. You only need it plausible — and the marginal evidence makes it more than plausible.Thorsten Meyer · The Labor Share · Post-Labor 02

Implications of Marginal Displacement Signals

This debate is vital because it influences policy decisions on ownership and income distribution. If AI is starting to shift value toward capital at the margins, it could justify policies promoting broad-based ownership to counteract potential inequality. Conversely, if the long-term aggregate remains stable, the urgency to overhaul existing structures diminishes. The current evidence suggests a cautious approach, recognizing that the signals of change are real but not yet conclusive.

AI Agents for Beginners: Build Your Digital Workforce with ChatGPT, No-Code Tools, and Automation

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Over the past 70 years, the US labor share has shown resilience, fluctuating within a narrow band despite multiple waves of technological innovation. Theories predicting a shift toward capital have faced the challenge of this long-term stability. Recent studies, however, highlight early displacement effects, especially among young workers in AI-affected roles, suggesting that the process may be in its initial stages. These signals are consistent with economic models that forecast a capital bias in AI technologies, but definitive proof remains elusive. The Labor Displacement Data: What Q1-Q2 2026 Actually Shows

“The core question is whether the early signals of displacement will translate into a long-term shift in the aggregate labor share.”

— Thorsten Meyer

Key Labor Market Indicators: Analysis with Household Survey Data (Streamlined Analysis with ADePT Software)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Unresolved Tensions Between Long-term Stability and Early Signals

It remains unclear whether the early displacement signals will lead to a sustained shift in the overall labor share. The data currently shows a stable aggregate over decades, but the recent localized effects suggest potential future change. The timing and scale of any shift are uncertain, and whether these marginal signals will accumulate into a systemic redistribution remains an open question.

Impacts of AI on Employment and Skills in Logistics

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Monitoring Data and Policy Responses to Early Displacement Signs

Researchers will continue tracking employment and income data at both the aggregate and disaggregated levels to assess whether the marginal signals intensify or dissipate. Policymakers may consider measures to support displaced workers and promote broad ownership structures as a precaution. The next wave of data in 2026 and beyond will be critical in determining whether the current signals develop into a long-term trend.

Modes of Thinking for Qualitative Data Analysis

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Key Questions

Is AI currently causing a decline in workers’ income share?

Not definitively. While aggregate data over 70 years shows stability, early signals at the margins—such as displacement among young, entry-level workers—suggest localized shifts that could indicate future changes.

Why is there disagreement among economists about this issue?

The disagreement centers on which signals are load-bearing: the long-term stable aggregate or the early, localized displacement effects. Both are supported by current data, but their implications differ.

What are the policy implications if AI begins shifting value toward capital?

Policies promoting broad-based ownership and income redistribution could become more urgent if AI’s impact on the labor share accelerates, but current evidence does not confirm a systemic shift yet.

How confident can we be about the future impact of AI on labor?

Confidence is limited because the evidence is ambiguous. The long-term aggregate data remains stable, but early signals suggest the process is in its initial stages, making future developments uncertain.

Source: ThorstenMeyerAI.com